Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

For those who have pondered about ways on how to start building credit, you are one of many who do not know where to start. Some leave school with skills to calculate equations, compose articles and understand modern technology but do not have a clue about their credit.

The funny thing is that having a good credit profile can make all the difference when it comes to making major financial moves in your life such as buying a house, purchasing a car, securing an apartment, applying for a small business loan, etc. Good credit will be proof for lenders that you are dependable and capable enough to handle money responsibly. However, a poor credit profile can ruin even easy-to-do financial plans.

Credti building does not mean you should be spending thousands and owning credit cards just like collectibles. Your credit profile is equivalent to a financial reputation. As much as it takes time for one to gain trust from other individuals, credit also requires time to develop with the lending organizations. This is great news as anyone can develop from scratch to create their credit history. You do not need to be rich, earn a lot of income, or be a financial guru to create your credit profile. All you need is to learn about the best practices involved in the process.

Most individuals tend to see credit as a means of borrowing funds from various companies. To me, it is a tool for attaining financial freedom through building a credit history. Developing a credit profile helps in saving thousands of dollars through reduced interest rates, easy approval of loans, and gaining access to top-notch financial products. For instance, consider two people buying similar cars; one with an excellent credit history and another with a poor one.

The connection between credit building and financial freedom is made even more apparent when bigger purchases come into play. When applying for a mortgage loan, business loans, or even looking for a new job, your lender or employer will look at your credit score and determine whether or not you’re a trustworthy borrower. Having an excellent credit score means having multiple options, choices, and being able to negotiate on terms. Good credit enables you to concentrate on prospects rather than the obstacles that might get in your way. In other words, building a great credit score isn’t about pleasing banks; it’s about giving yourself the choice.

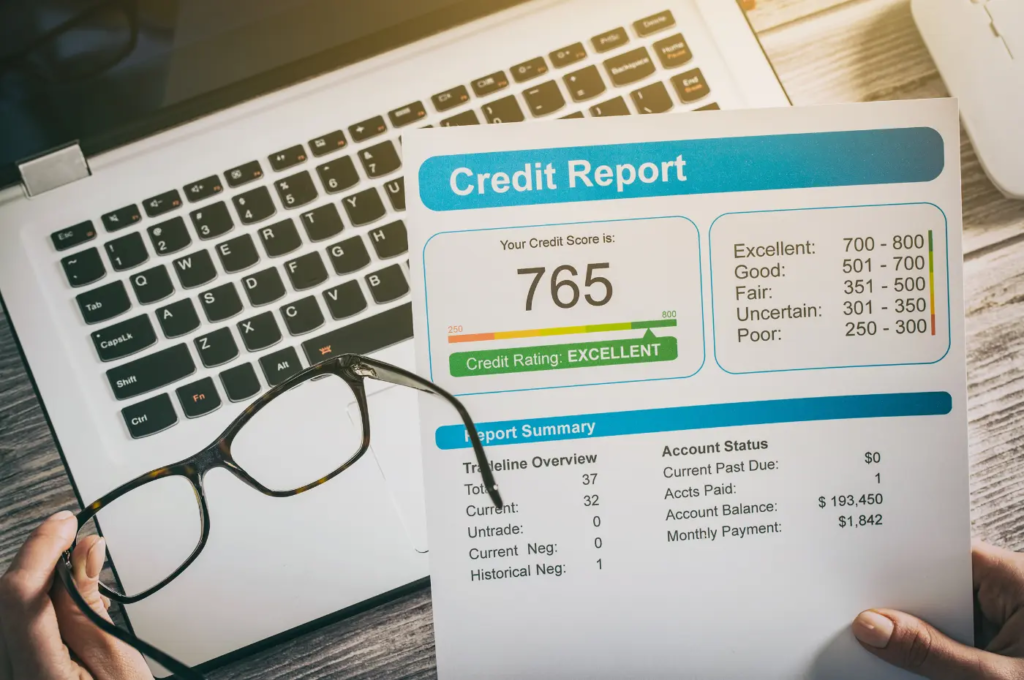

It may be beneficial to have a brief understanding of what lenders look for before going over practical advice. A variety of elements are considered by the credit scoring algorithm used by most financial institutions when determining a credit score. Your payment history, credit utilization rate, account tenure, new credit applications, and credit mix are among these considerations. According to the FICO system, the most important element of your score is payment history, which constitutes around 35% of it. Credit utilization rate comes next at approximately 30%.

| Factor | Approximate Impact |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Length of Credit History | 15% |

| New Credit | 10% |

| Credit Mix | 10% |

With the knowledge gained, I have come to realize that it pays more to focus on fundamentals rather than quick fixes or hacks to improve your credit scores. In many instances, paying your bills regularly, keeping your debts under control, and ensuring you keep your credit active are more effective approaches than some of those overly complicated strategies you might come across online. Consistency seems to carry a lot of weight in the credit world and it is important factor to consider for financial freedom.

Perhaps one of the most straightforward ways to answer the question, “How to start building credit?” is by getting yourself a secured credit card. It works by requiring you to make a security deposit that will serve as your credit limit. With a $300 security deposit, you are likely to get a $300 credit limit on the card.

At first, I assumed there must be something wrong with a secured credit card. After all, it would probably not be called a secured card if it was superior to a standard card. However, a secured credit card is like training wheels for the financial bicycle. The trick here is to use the credit card for small expenses and pay the whole sum back at the end of each month. Consider it a way to borrow a little money just to show that you are financially responsible. Gradually, many companies offering secured cards will switch to unsecured cards, and they are the perfect option to start credit building history.

First of all, secured credit cards have limits. Your spending will be restricted to the amount you deposited into the bank. Hence, the probability of getting too far is minimal. Instead of seeing the deposit as lost money, consider it an investment in your financial future since you will get benefits from it later on.

Credit building loans represent another great option for creating positive credit history. It is different from regular loans because you won’t get any money upfront. Instead, the funds are put into a secured account, and you repay the loan in monthly installments. When it is repaid, you can withdraw your money.

At first glance, this might seem rather odd. But the reason why it is done is quite clear; each on-time payment is reported by the credit bureaus. In other words, this can be thought of as a method of creating a positive payment record. Credit builder loans are thus particularly useful for people without any kind of credit history.

One lesser known way on how to start building credit is to obtain a secondary status, known as an authorized user, on another person’s credit card. As mentioned above, this can help you to build up some credit history from your relationship with another individual who has been managing a credit card for years.

It is important to note that the key word in this approach is “trusted.” There is nothing worse than piggybacking on the credit report of someone who never pays on time and always carries high balances on their cards. This method may also be likened to joining a successful sports team. The good reputation of the team works in your favor, but only if you consistently perform well enough to maintain it. Although being an authorized user does not have to be your only means of building credit, it will certainly help if you are able to manage your own personal credit responsibility accordingly.

Perhaps the one habit that can greatly impact your credit rating involves paying all your bills on time. As per FICO, your payment history accounts for about 35% of the factors in your credit score computation – the highest weightage among them all. Missing even just one payment is enough to negatively affect your score.

For me, payment history represents your financial report card. Creditors need assurance that you are reliable in fulfilling your obligations moving forward. Each on-time payment builds confidence. Late payments, on the other hand, undermine this effort. There are numerous tools available online to help you avoid missing payment deadlines, including automatic payments, calendars, budgeting apps, and others. You are now armed with the means to keep track of your payments through technology.

Even recent financial research still points out that the most crucial indicator when predicting an individual’s willingness to pay back loans is the individual’s payment history. The credit score system gives a considerable amount of importance to consistent repayments since past behavior determines future behavior.

The takeaway is clear. When you can do just one thing, make sure to prioritize your timely repayments. It might not be fancy, but it gets the job done.

The utilization of credit is simply the measure of how much of your credit line you have used. So when your credit limit is $1,000 and you owe $300, then your utilization is at 30%. Experts advise keeping below this percentage whenever possible. Many creditors want under 10% for best scoring results.

Utilization that is high can be interpreted as a sign that you depend too heavily on loans. Even if you pay back on time, being maxed out on credit cards can lower your score. My advice is always to think of your credit limit as a pool of water. Just because the pool can hold much more does not mean that you fill it up to the rim each day.

Getting acquainted with the process of how to get credit scores is crucial when managing finances. Getting your credit scores will be helpful in discovering any mistake on your reports, any instances of fraud, and even your progress. Consumers who have obtained their reports are usually amazed to find discrepancies, which could be anything from incorrect account balances and balances to having accounts which are not theirs.

By regularly checking your reports, you will easily notice errors and solve them accordingly. It is similar to having a regular check-up done in your body. You should not wait for yourself to fall ill before consulting with a doctor because of this. Monitoring your report frequently can help you fix errors and even analyze certain trends which could give you a clear insight of financial freedom.

Personal information that is not accurate is quite common along with duplicate entries. Some other errors which may affect your score include having incorrect payments status and wrong account balances.

A common misconception about financial management is that closing old credit cards always works to your advantage. Actually, closing old credit cards may work against you. The age of these accounts helps determine the length of your average credit history, which is considered in calculating your credit score.

As long as an old credit card doesn’t have annual charges, it may be preferable to keep it active. I liken my old credit accounts to mature trees in a garden setting. While they may not be as showy as young ones, they root the whole setting firmly. Longer credit histories reflect stability, which most lenders prefer.

Applying for too many different forms of credit in a short time is seen negatively by most lenders. With each application, you are bound to have a hard inquiry on your report, which can lower your credit score. Even one single hard inquiry won’t significantly lower your score, but several may cause problems.

Patience is a virtue worth learning in personal finance management. Don’t apply for every credit offer coming into your email inbox or regular mail box. Use only when necessary and the product suits your needs financially. Being a responsible borrower means you have matured and thought ahead, qualities that build better credit in the future.

Having debts is not always wrong because being smart about managing your debt could actually improve your credit score. The problem starts when debts are too much for you to handle. It is always better to pay off your high-interest debts since it helps reduce financial worries and your credit utilization.

This is how I usually deal with it. You should always start by paying off high-interest debts while making minimum payments to other debts. It makes you pay less in interest while getting rid of more debts faster. And when there are fewer debts to worry about, the better your credit score will be.

One of my main realizations about credit strong usage is the fact that emotions and credit cards never mix well. Stress, excitement, boredom, or impulsivity are likely to trigger reckless spending. Rational credit management involves the understanding that credit should not be viewed as free cash.

Consider whether an expense meets a need or satisfies a momentary desire before paying with your card. This will help you avoid spending that leads to unwanted debt. In many cases, good credit ratings result from numerous smaller steps.

Even the best strategy for credit building fails when common mistakes occur. They include:

There are people who spend several months on credit repair efforts that get ruined due to preventable errors. Building up credit is like cultivating a garden. It needs a lot of time but can ruin easily.

When you have no idea where to start, try the following strategy:

By adhering to the above guidelines, you can ensure that your credit building efforts yield successful results in the long run. While it takes some time to improve your credit score, persistence is bound to bring amazing results.

The knowledge of how to start building credit from scratch is an extremely useful skill to acquire. By having good credit, you will have more options at your disposal, including access to better interest rates and more favorable loan conditions. The process of achieving credit strong and financial freedom does not require perfection. Consistency is the key. All good decisions that are related to finance will positively impact your reputation as a borrower in the future. Using the recommendations from this manual, you will be able to improve your credit rating, learn how to get credit score improvements organically, and create a prosperous future for yourself.

Most people begin seeing credit activity within a few months, but building strong credit often takes six months to several years of consistent positive behavior.

A secured credit card combined with on-time payments is one of the fastest and safest methods for beginners.

Yes. Credit builder loans, authorized user status, and certain loan products can help establish credit history.

While scoring models vary, a score above 670 is generally considered good, with higher scores providing access to better lending terms.

No. Checking your own credit score is considered a soft inquiry and does not negatively impact your credit profile.

Share your details, and we will get back to you shortly!

This will close in 0 seconds

Share your details, and we will get back to you shortly!

This will close in 0 seconds